Probabilistic thinking is essentially trying to estimate, using some tools of math and logic, the likelihood of any specific outcome coming to pass. It is one of the best tools we have to improve the accuracy of our decisions. In a world where each moment is determined by an infinitely complex set of factors, probabilistic thinking helps us identify the most likely outcomes. When we know these our decisions can be more precise and effective.

** The Great Mental Models encyclopedia series is out. **

Are you going to get hit by lightning or not?

Why we need the concept of probabilities at all is worth thinking about. Things either are or are not, right? We either will get hit by lightning today or we won’t. The problem is, we just don’t know until we live out the day, which doesn’t help us at all when we make our decisions in the morning. The future is far from determined and we can better navigate it by understanding the likelihood of events that could impact us.

Our lack of perfect information about the world gives rise to all of probability theory, and its usefulness. We know now that the future is inherently unpredictable because not all variables can be known and even the smallest error imaginable in our data very quickly throws off our predictions. The best we can do is estimate the future by generating realistic, useful probabilities. So how do we do that?

Probability is everywhere, down to the very bones of the world. The probabilistic machinery in our minds—the cut-to-the-quick heuristics made so famous by the psychologists Daniel Kahneman and Amos Tversky—was evolved by the human species in a time before computers, factories, traffic, middle managers, and the stock market. It served us in a time when human life was about survival, and still serves us well in that capacity.

But what about today—a time when, for most of us, survival is not so much the issue? We want to thrive. We want to compete, and win. Mostly, we want to make good decisions in complex social systems that were not part of the world in which our brains evolved their (quite rational) heuristics.

For this, we need to consciously add in a needed layer of probability awareness. What is it and how can I use it to my advantage?

There are three important aspects of probability that we need to explain so you can integrate them into your thinking to get into the ballpark and improve your chances of catching the ball:

- Bayesian thinking,

- Fat-tailed curves

- Asymmetries

Thomas Bayes and Bayesian thinking: Bayes was an English minister in the first half of the 18th century, whose most famous work, “An Essay Toward Solving a Problem in the Doctrine of Chances” was brought to the attention of the Royal Society by his friend Richard Price in 1763—two years after his death. The essay, the key to what we now know as Bayes’s Theorem, concerned how we should adjust probabilities when we encounter new data.

The core of Bayesian thinking (or Bayesian updating, as it can be called) is this: given that we have limited but useful information about the world, and are constantly encountering new information, we should probably take into account what we already know when we learn something new. As much of it as possible. Bayesian thinking allows us to use all relevant prior information in making decisions. Statisticians might call it a base rate, taking in outside information about past situations like the one you’re in.

Consider the headline “Violent Stabbings on the Rise.” Without Bayesian thinking, you might become genuinely afraid because your chances of being a victim of assault or murder is higher than it was a few months ago. But a Bayesian approach will have you putting this information into the context of what you already know about violent crime.

You know that violent crime has been declining to its lowest rates in decades. Your city is safer now than it has been since this measurement started. Let’s say your chance of being a victim of a stabbing last year was one in 10,000, or 0.01%. The article states, with accuracy, that violent crime has doubled. It is now two in 10,000, or 0.02%. Is that worth being terribly worried about? The prior information here is key. When we factor it in, we realize that our safety has not really been compromised.

Conversely, if we look at the diabetes statistics in the United States, our application of prior knowledge would lead us to a different conclusion. Here, a Bayesian analysis indicates you should be concerned. In 1958, 0.93% of the population was diagnosed with diabetes. In 2015 it was 7.4%. When you look at the intervening years, the climb in diabetes diagnosis is steady, not a spike. So the prior relevant data, or priors, indicate a trend that is worrisome.

It is important to remember that priors themselves are probability estimates. For each bit of prior knowledge, you are not putting it in a binary structure, saying it is true or not. You’re assigning it a probability of being true. Therefore, you can’t let your priors get in the way of processing new knowledge. In Bayesian terms, this is called the likelihood ratio or the Bayes factor. Any new information you encounter that challenges a prior simply means that the probability of that prior being true may be reduced. Eventually, some priors are replaced completely. This is an ongoing cycle of challenging and validating what you believe you know. When making uncertain decisions, it’s nearly always a mistake not to ask: What are the relevant priors? What might I already know that I can use to better understand the reality of the situation?

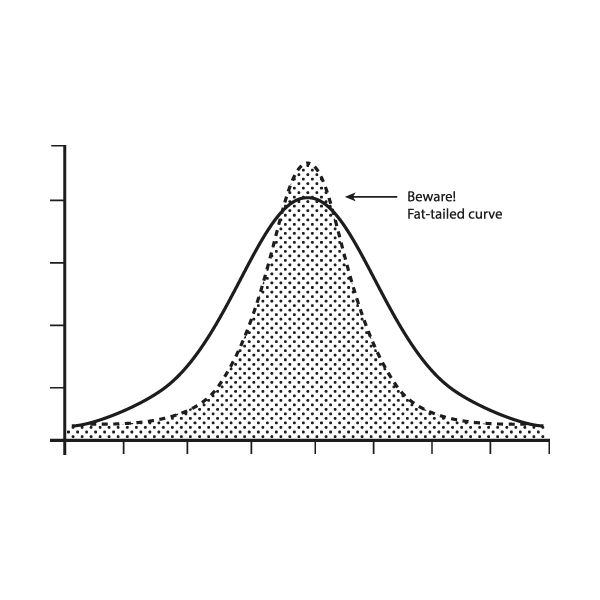

Now we need to look at fat-tailed curves: Many of us are familiar with the bell curve, that nice, symmetrical wave that captures the relative frequency of so many things from height to exam scores. The bell curve is great because it’s easy to understand and easy to use. Its technical name is “normal distribution.” If we know we are in a bell curve situation, we can quickly identify our parameters and plan for the most likely outcomes.

Fat-tailed curves are different. Take a look.

At first glance they seem similar enough. Common outcomes cluster together, creating a wave. The difference is in the tails. In a bell curve the extremes are predictable. There can only be so much deviation from the mean. In a fat-tailed curve there is no real cap on extreme events.

The more extreme events that are possible, the longer the tails of the curve get. Any one extreme event is still unlikely, but the sheer number of options means that we can’t rely on the most common outcomes as representing the average. The more extreme events that are possible, the higher the probability that one of them will occur. Crazy things are definitely going to happen, and we have no way of identifying when.

Think of it this way. In a bell curve type of situation, like displaying the distribution of height or weight in a human population, there are outliers on the spectrum of possibility, but the outliers have a fairly well defined scope. You’ll never meet a man who is ten times the size of an average man. But in a curve with fat tails, like wealth, the central tendency does not work the same way. You may regularly meet people who are ten, 100, or 10,000 times wealthier than the average person. That is a very different type of world.

Let’s re-approach the example of the risks of violence we discussed in relation to Bayesian thinking. Suppose you hear that you had a greater risk of slipping on the stairs and cracking your head open than being killed by a terrorist. The statistics, the priors, seem to back it up: 1,000 people slipped on the stairs and died last year in your country and only 500 died of terrorism. Should you be more worried about stairs or terror events?

Some use examples like these to prove that terror risk is low—since the recent past shows very few deaths, why worry?[1] The problem is in the fat tails: The risk of terror violence is more like wealth, while stair-slipping deaths are more like height and weight. In the next ten years, how many events are possible? How fat is the tail?

The important thing is not to sit down and imagine every possible scenario in the tail (by definition, it is impossible) but to deal with fat-tailed domains in the correct way: by positioning ourselves to survive or even benefit from the wildly unpredictable future, by being the only ones thinking correctly and planning for a world we don’t fully understand.

Asymmetries: Finally, you need to think about something we might call “metaprobability” —the probability that your probability estimates themselves are any good.

This massively misunderstood concept has to do with asymmetries. If you look at nicely polished stock pitches made by professional investors, nearly every time an idea is presented, the investor looks their audience in the eye and states they think they’re going to achieve a rate of return of 20% to 40% per annum, if not higher. Yet exceedingly few of them ever attain that mark, and it’s not because they don’t have any winners. It’s because they get so many so wrong. They consistently overestimate their confidence in their probabilistic estimates. (For reference, the general stock market has returned no more than 7% to 8% per annum in the United States over a long period, before fees.)

Another common asymmetry is people’s ability to estimate the effect of traffic on travel time. How often do you leave “on time” and arrive 20% early? Almost never? How often do you leave “on time” and arrive 20% late? All the time? Exactly. Your estimation errors are asymmetric, skewing in a single direction. This is often the case with probabilistic decision-making.[2]

Far more probability estimates are wrong on the “over-optimistic” side than the “under-optimistic” side. You’ll rarely read about an investor who aimed for 25% annual return rates who subsequently earned 40% over a long period of time. You can throw a dart at the Wall Street Journal and hit the names of lots of investors who aim for 25% per annum with each investment and end up closer to 10%.

The spy world

Successful spies are very good at probabilistic thinking. High-stakes survival situations tend to make us evaluate our environment with as little bias as possible.

When Vera Atkins was second in command of the French unit of the Special Operations Executive (SOE), a British intelligence organization reporting directly to Winston Churchill during World War II[3], she had to make hundreds of decisions by figuring out the probable accuracy of inherently unreliable information.

Atkins was responsible for the recruitment and deployment of British agents into occupied France. She had to decide who could do the job, and where the best sources of intelligence were. These were literal life-and-death decisions, and all were based in probabilistic thinking.

First, how do you choose a spy? Not everyone can go undercover in high-stress situations and make the contacts necessary to gather intelligence. The result of failure in France in WWII was not getting fired; it was death. What factors of personality and experience show that a person is right for the job? Even today, with advancements in psychology, interrogation, and polygraphs, it’s still a judgment call.

For Vera Atkins in the 1940s, it was very much a process of assigning weight to the various factors and coming up with a probabilistic assessment of who had a decent chance of success. Who spoke French? Who had the confidence? Who was too tied to family? Who had the problem-solving capabilities? From recruitment to deployment, her development of each spy was a series of continually updated, educated estimates.

Getting an intelligence officer ready to go is only half the battle. Where do you send them? If your information was so great that you knew exactly where to go, you probably wouldn’t need an intelligence mission. Choosing a target is another exercise in probabilistic thinking. You need to evaluate the reliability of the information you have and the networks you have set up. Intelligence is not evidence. There is no chain of command or guarantee of authenticity.

The stuff coming out of German-occupied France was at the level of grainy photographs, handwritten notes that passed through many hands on the way back to HQ, and unverifiable wireless messages sent quickly, sometimes sporadically, and with the operator under incredible stress. When deciding what to use, Atkins had to consider the relevancy, quality, and timeliness of the information she had.

She also had to make decisions based not only on what had happened, but what possibly could. Trying to prepare for every eventuality means that spies would never leave home, but they must somehow prepare for a good deal of the unexpected. After all, their jobs are often executed in highly volatile, dynamic environments. The women and men Atkins sent over to France worked in three primary occupations: organizers were responsible for recruiting locals, developing the network, and identifying sabotage targets; couriers moved information all around the country, connecting people and networks to coordinate activities; and wireless operators had to set up heavy communications equipment, disguise it, get information out of the country, and be ready to move at a moment’s notice. All of these jobs were dangerous. The full scope of the threats was never completely identifiable. There were so many things that could go wrong, so many possibilities for discovery or betrayal, that it was impossible to plan for them all. The average life expectancy in France for one of Atkins’ wireless operators was six weeks.

Finally, the numbers suggest an asymmetry in the estimation of the probability of success of each individual agent. Of the 400 agents that Atkins sent over to France, 100 were captured and killed. This is not meant to pass judgment on her skills or smarts. Probabilistic thinking can only get you in the ballpark. It doesn’t guarantee 100% success.

There is no doubt that Atkins relied heavily on probabilistic thinking to guide her decisions in the challenging quest to disrupt German operations in France during World War II. It is hard to evaluate the success of an espionage career, because it is a job that comes with a lot of loss. Atkins was extremely successful in that her network conducted valuable sabotage to support the allied cause during the war, but the loss of life was significant.

Conclusion

Successfully thinking in shades of probability means roughly identifying what matters, coming up with a sense of the odds, doing a check on our assumptions, and then making a decision. We can act with a higher level of certainty in complex, unpredictable situations. We can never know the future with exact precision. Probabilistic thinking is an extremely useful tool to evaluate how the world will most likely look so that we can effectively strategize.

References:

[1] Taleb, Nassim Nicholas. Antifragile. New York: Random House, 2012.

[2] Bernstein, Peter L. Against the Gods: The Remarkable Story of Risk. New York: John Wiley and Sons, 1996. (This book includes an excellent discussion in Chapter 13 on the idea of the scope of events in the past as relevant to figuring out the probability of events in the future, drawing on the work of Frank Knight and John Maynard Keynes.)

[3] Helm, Sarah. A Life in Secrets: The Story of Vera Atkins and the Lost Agents of SOE. London: Abacus, 2005.